- Dollar gains as ISM mfg. new orders beat estimates

- Pound traders await Thursday’s BoE decision

- Aussie the main loser after RBA stands pat

- and Nasdaq close in the red, oil hits new three-month high

Improving manufacturing outlook helps the dollar

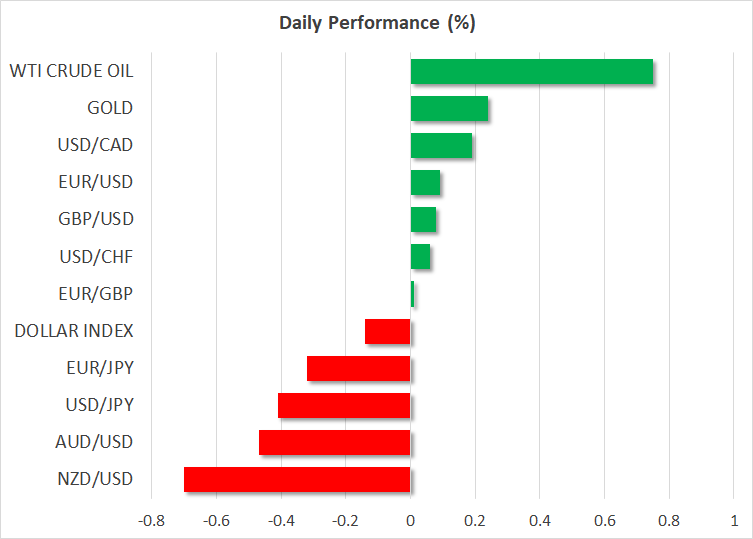

The US dollar traded higher against all the other major currencies on Tuesday, but today it seems to be stabilizing, properly extending winnings only against the risk-linked currencies, the , and .

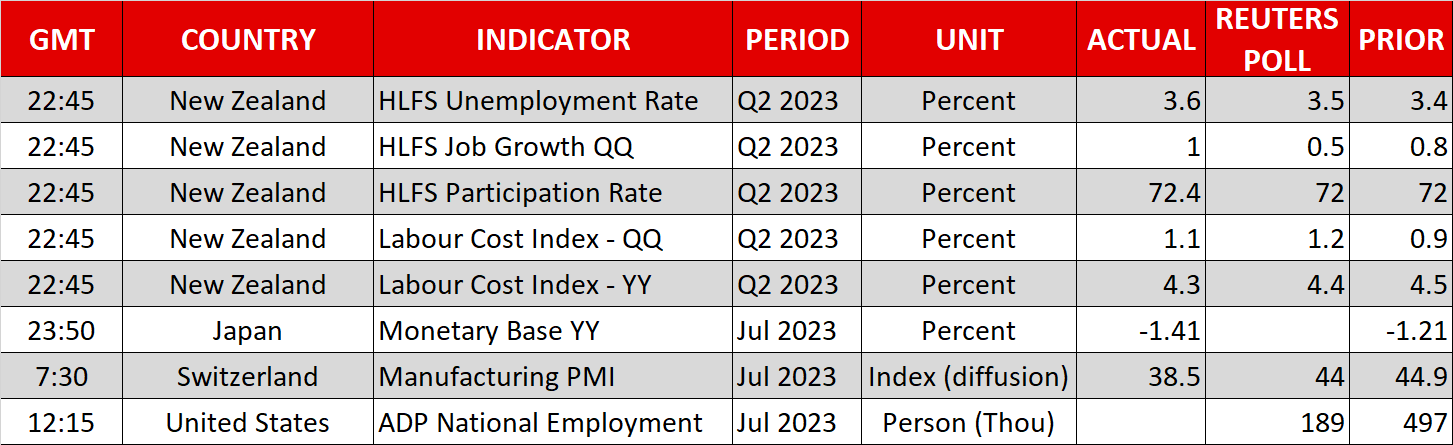

What may have allowed traders to buy some more dollars yesterday was the ISM manufacturing PMI for July. The index improved to 46.4 from 46.0, and although this was still below analysts’ estimate of 46.8, the new orders subindex came in much better than anticipated. It rose to 47.3 from 45.6, while the forecast was for a drop to 44.0.

An improving orders outlook amid the drag from higher borrowing costs translates into improving demand for goods, which could eventually prompt businesses to increase production, which corroborates the soft-landing narrative.

Alongside the dollar, US Treasury yields also marched higher, with the 10-year yield poking its nose above 4.05% for the first time since July 10, although they pulled back today after Fitch unexpectedly downgraded the US government’s top credit rating.

That said, expectations with regards to the Fed’s future course of action were barely changed. Investors remained convinced that the Fed had already concluded its own tightening crusade last week and that a series of rate reductions are likely to be appropriate during 2024.

The data set that could make them consider another hike this year and less cuts thereafter may be Friday’s jobs report for July. However, investors will have the opportunity to proceed with an early evaluation of how the labor market fared during the month when they get the ADP employment report today, while Thursday’s ISM non-manufacturing PMI could offer more insights with regards to business activity.

Pound awaits BoE, aussie suffers after RBA

With most major central banks already seen ending or approaching the end of their tightening campaigns, the only one standing out is the Bank of England, which meets tomorrow. Following the larger-than-expected slowdown in UK inflation for June, investors see a larger probability of a 25bps hike rather than another double one, but they are also anticipating around 60bps worth of additional increments thereafter.

Therefore, even if the BoE hikes by 25bps and disappoints those expecting more, a hawkish message that allows traders to maintain rate hike bets for the coming months, could keep pound/dollar in an uptrend mode for a while longer.

The aussie was yesterday’s main loser, suffering after the RBA decided to remain sidelined for a second straight meeting, offering no signals on whether another rate hike would be appropriate.

Today, the most wounded currency is the kiwi, which came under pressure after New Zealand’s jobs data revealed that the nation’s unemployment rate rose by more than expected.

Equities pull back, oil extends rally

The S&P 500 and the Nasdaq closed in the red yesterday, perhaps due to new-month rebalancing or because investors have begun locking some profits ahead of more key earnings and important US data, like Friday’s jobs report.

Wall Street finished July on a strong footing as investors cheered better-than-expected earnings, but also data pointing to a resilient US economy at a time when inflation is cooling. With investors believing that the Fed has already ended this hiking cycle and expecting a series of rate reductions, the uptrends on Wall Street may be destined to continue for a while longer, unless Friday’s employment report comes in so strong that it prompts participants to start drastically scaling back their rate-cut bets.

Oil prices extended their summer rally, hitting a fresh three-month high due to signs of tightening supply as Saudi Arabia is expected to extend its voluntary cuts into September. Saudi’s production shrank by 860k barrels per day (bpd) last month, while total OPEC output was down 840k bpd.

คำแนะนำการอ่านบทความนี้ : บางบทความในเว็บไซต์ ใช้ระบบแปลภาษาอัตโนมัติ คำศัพท์เฉพาะบางคำอาจจะทำให้ไม่เข้าใจ สามารถเปลี่ยนภาษาเว็บไซต์เป็นภาษาอังกฤษ หรือปรับเปลี่ยนภาษาในการใช้งานเว็บไซต์ได้ตามที่ถนัด บทความของเรารองรับการใช้งานได้หลากหลายภาษา หากใช้ระบบแปลภาษาที่เว็บไซต์ยังไม่เข้าใจ สามารถศึกษาเพิ่มเติมโดยคลิกลิ้งค์ที่มาของบทความนี้ตามลิ้งค์ที่อยู่ด้านล่างนี้

Source link