Good morning. It is a pleasure to be back in Michigan, although I wish I had been here to participate in the Turkey Trot last week, which is an annual tradition for my family and me. It is especially a treat to be back in Detroit, with its rich history of music, art, architecture, and industrial innovation—which I will address today. I am also delighted to see some familiar faces.

Today, I would like to discuss the economic outlook and focus on one particularly important aspect of the economy: productivity. I have spent much of my career researching the ways in which American ingenuity and invention can be wellsprings of economic growth. I am here, therefore, to address the impressive innovation happening in the auto industry and what it tells us about future prospects for productivity in the U.S. manufacturing sector and in the economy more generally. I can think of no better place to do that than in the Motor City.

Outlook

To set the stage, I will first turn to the U.S. economy as a whole, where inflation remains much too high. As a result, the Federal Reserve must continue to focus on bringing inflation back down to our 2 percent target.

We have begun to see some improvement in the inflation data. The October report on consumer prices was encouraging, particularly the slowing in core inflation—the measure that excludes more volatile categories, such as food and energy. Producer price inflation also moderated in October, suggesting that inflation pressures on businesses may be easing. Nonetheless, I would be cautious about reading too much into one month of relatively favorable data.

Core goods inflation has finally begun to slow significantly, helped by some long-anticipated improvement in global supply chains. Declines in wholesale prices for used cars and in prices for key manufacturing components, like plastic resin and steel, also suggest continued moderation in goods price inflation.

Services, however, make up about two-thirds of consumer spending, and inflation in that sector has not yet slowed. Notably, inflation in housing costs shot up this year and will likely contribute substantially to overall inflation for some time. Nonetheless, some good news is emerging on this front. Rent increases on new leases have slowed in recent months. And a substantial number of multifamily units currently under construction will be delivered next year, helping to ease the housing shortage. Still, these positive developments are likely to feed into measured consumer prices only gradually.

Services prices more broadly have accelerated sharply this year and may prove to be a persistent factor keeping inflation elevated. Demand for services continues to recover from its pandemic lows, with the release of pent-up demand for travel evident to anyone who has spent much time in DTW and other airports recently.

Labor compensation is a key factor for non-housing services prices, and growth in labor costs remains well above pre-pandemic rates. There has been some moderation recently, with slowing in average hourly earnings and in the employment cost index. But wage growth remains above what would be consistent with 2 percent inflation, given prevailing trends in productivity growth.

Productivity

In Michigan and the other parts of the country that boast manufacturing hubs, we all understand the importance of productivity. Productivity growth is a key factor in the health of the overall economy and in the daily lives of all Americans. Because ultimately, it drives rising standards of living for all of us.

Growth in labor productivity, or output per hour worked, has been lackluster in the U.S. economy and around the world in recent years.1 Some observers fret that we are running out of innovative ideas to squeeze more outputs from the same inputs.2 Others look around and see amazing technology used in cutting-edge factories, warehouses, and stores and wonder if the innovation is happening but not spreading as fast as it once did. Whatever the cause, in recent years output per hour has only increased at half the rate it did as recently as the mid-2000s. This is cause for concern.

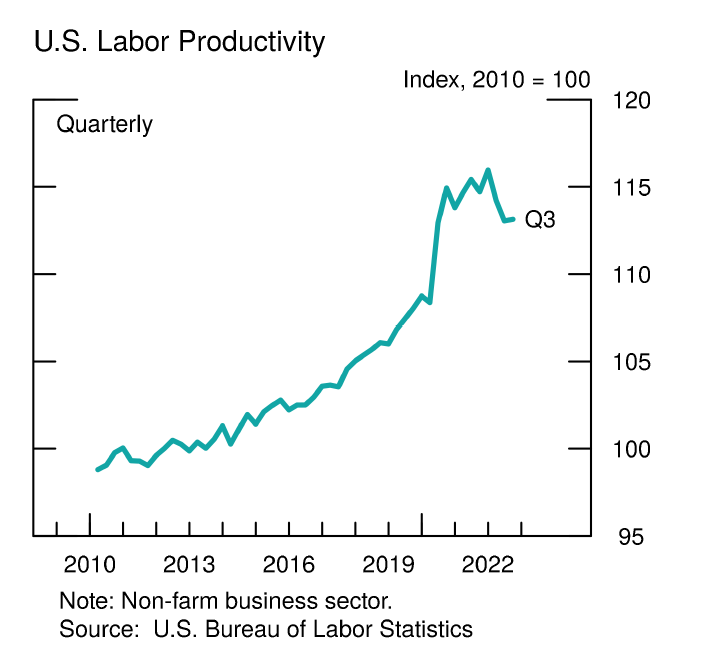

Over the first three quarters of 2022, productivity in the business sector has recorded a disappointing decline of 3-3/4 percent at an annual rate. Payroll employment in the private sector has continued to increase, yet gross domestic product (GDP) has done little more than move sideways, resulting in an outright decline in labor productivity. However, the recent decline in productivity is partly an artifact of the pandemic. In 2020 and 2021, productivity soared when firms found ways to keep producing while many employees were away from the workplace (figure 1). Meanwhile, the economy shifted away from services—a lower-productivity sector—and toward goods—a higher-productivity sector—as households substituted new televisions for dining out and family vacations. As a result, average productivity moved up. These temporary changes have largely reversed, leading to the recent declines in productivity, pushing it back toward its pre-pandemic trend. The tight labor market has played a role, as well. With 1.8 job openings for every job seeker, firms may be using the GDP slowdown as an opportunity to let their hiring catch up to the earlier surge in labor demand. Some firms may even be operating with a larger workforce than necessary in order to hold on to talent they may not have retained in normal times.

In any event, we should avoid making too much of quarterly swings in choppy data but focus instead on the trend over several years. Taking this longer view, what pace of productivity growth should we expect going forward? This question is critical to policymakers, as inflation is tied to productivity. When firms see rising output per hour, they have room to keep prices low. For consumer goods, this can help lower inflation. For material inputs, this lowers the cost of downstream production. And for equipment, lower prices mean more capital investment, a knock-on effect that boosts productivity further.

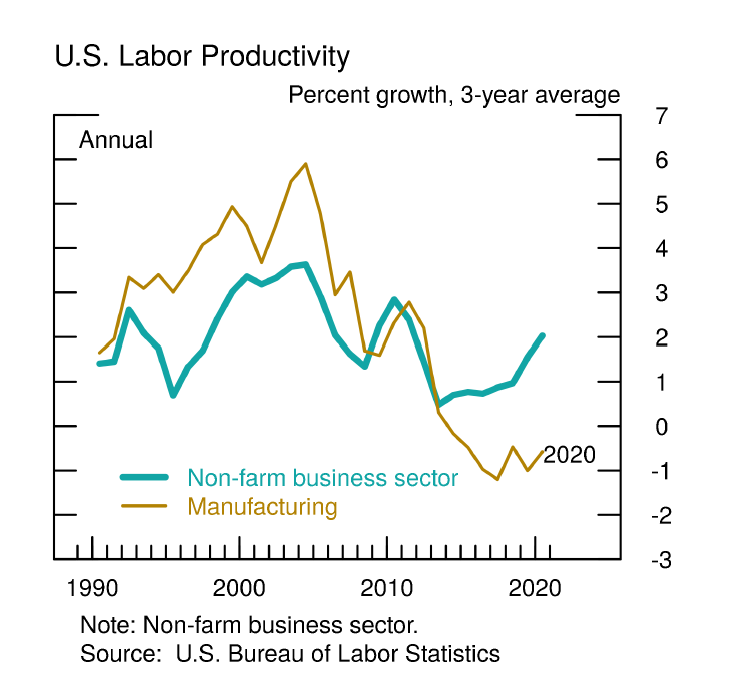

If there is a productivity revival, it will likely involve manufacturing, if history is our guide. When it comes to productivity, the sector has a record of punching above its weight. Since the mid-20th century, manufacturing productivity has risen a full percentage point faster than productivity for the broader economy (figure 2). The sector seems to find ways to do more with less. For example, manufacturing lost a staggering 5 million workers from 2000 to 2019, nearly 40 percent of its workforce. As seen in Michigan, this meant difficult transitions for industrial workers and their families as the economy shifted toward services and substituted imports for domestic production. Yet, at the same time, output as measured by the Federal Reserve’s industrial production index continued to climb.

Since the mid-2010s, though, this relationship has reversed, and manufacturing productivity has been noticeably lower than that of the overall economy. What explains the anemic growth in recent years? For one thing, IT equipment manufacturing has moved offshore, taking the productivity gains from progressively smaller and faster computer chips with it.3 More generally, offshore locations have focused on production of high-volume goods. Many of the remaining U.S. plants produce more specialized products, which tend to require more specialized labor and have lower productivity growth.4

The motor vehicle industry has mostly defied this trend of offshoring final production. The U.S. motor vehicle industry still produces more than 10 million vehicles a year and employs 1 million people at assembly plants, labs, and suppliers. Furthermore, it is an extremely innovative industry, and fierce competition forces automakers to roll out innovations quickly. Dozens of motor vehicle research and development labs reside in Michigan alone, churning out ideas for vehicle safety, fuel efficiency, comfort, and style. And with each passing year, cars and trucks look more like computers on wheels.

Looking around Michigan today, I see all kinds of changes. Some changes are to the production process, like the newest generation of robots. These communicate at lightning speed, using the same high-speed “5G” technology as the latest phones; utilize artificial intelligence to adapt to their environment; and operate safely right next to workers on the assembly line. Some changes are to design, like collision avoidance systems, sophisticated navigation apps, and the dozens of electric vehicles now on the road or coming to market soon.

Some observers look at these changes with trepidation. Robot orders surged after the onset of the pandemic and have continued apace, a partial solution to the critical shortage of labor in manufacturing.5 What does all this mean for production line workers? Motor vehicle manufacturers have been the most intensive users of robots for decades. The first assembly line robot was rolled out in 1961 by General Motors in Trenton, New Jersey. Yet, the motor vehicle industry still employs more than 1 million workers, and its share of manufacturing employment has been going up since 2010. How did that happen? Research has shown that workers are not just suited for a single job—they have a bundle of broadly applicable skills. When robots take over one task, workers are shifted to another task and, in turn, new tasks appear.6 The set of tasks to perform is not fixed, a belief economists call the “lump of labor fallacy.” Rather, we need production workers to work with the new equipment and to focus on the problem-solving that robots do not do well. That means that the next generation of plant workers will use touch screens a lot more and rivet guns a lot less.

And the systems they install as they assemble the vehicles are more laden with electronics with each passing year. Many are anticipating the arrival of the self-driving car, but in some respects, it is already here. Vehicles can parallel park themselves with the touch of a button, stop you from drifting out of your lane, and follow the car ahead of you, keeping a safe distance.

While the U.S. is not making as many semiconductor chips anymore, we are using a lot of them. If that was not apparent already, we learned that lesson the hard way during the pandemic. I understand that, even now, thousands of vehicles are all but built, parked while they await missing chips. The increasing share of electronic content in vehicles contributes to that delay, as does the shift toward electric vehicles, which may have two or three times the chip content of an internal combustion vehicle. The shortfalls in supply and corresponding price pressures have eased somewhat, but they have not disappeared.

Highly innovative companies in the motor vehicle industry—as well as pharmaceuticals, biotechnology, and, of course, information technology—stand out as leaders in driving the quality of goods up and the cost of production down. Why isn’t that showing up in productivity? For one thing, it takes time. History has shown that major innovations take years for their effects to be fully manifested. Firms have to reorganize production—including changing the layout of plants, rethinking management, and reshuffling workers—to maximize their talents.7 Electrification of the manufacturing sector took decades as plants were redesigned and rebuilt to exploit the flexibility of getting away from steam power.8 Likewise, we still have not seen the last of the changes that the IT revolution will bring.

Productivity-enhancing ideas spread more quickly in more dynamic environments. When labor and capital move quickly toward their best uses—at the more productive firms—overall productivity accelerates. And when firms have close competitors on their heels, they may adopt new techniques faster.9 Entrepreneurship plays an important role in this process. Sometimes, a new idea needs a new firm not committed to old ways of doing business. This kind of dynamism has diminished in recent years, though the surge in business creation in the past two years may be an encouraging sign.10

Indeed, the U.S. manufacturing sector is healthy. The recovery from the pandemic downturn has been remarkable, especially in comparison to the Great Recession. The sector is currently producing at 3 percent above its pre-pandemic level. And, importantly, October marked 18 consecutive months of increasing manufacturing employment. If manufacturing were to return to its role as a productivity leader, productivity for the total economy would grow noticeably faster.

Looking ahead, productivity plays an important role in our thinking about the outlook. Productivity growth raises the nation’s per capita income and, one hopes, the welfare of the typical household. As I mentioned earlier, productivity growth may also help lower prices. If we can make more with less, firms can lower the cost of the final product and still remain profitable. For this reason, it is heartening to see all the innovation happening in the motor vehicle industry and throughout the economy. It is hard to know exactly when all the benefits will show up, but we know the historical evidence suggests they are coming.

Policy Implications

What does all this mean for monetary policy? Innovation and productivity growth undergird our long-term growth prospects, but they have only an indirect link to current inflation developments. More broadly, the auto sector and manufacturing overall serve as a microcosm to observe many factors buffeting the economy and impacting consumer prices, such as bottlenecks and labor shortages. Notwithstanding some easing of these pressures on goods prices, services prices continue to rise briskly. Altogether, inflation is still unacceptably high and must be our primary focus.

The Federal Reserve has taken significant steps to rein in price increases. Since March, the Federal Open Market Committee (FOMC) has raised its policy rate nearly 4 percentage points, an unusually rapid pace of increases that has significantly tightened financial conditions. That tightening is clearly slowing demand in sectors that are interest sensitive, especially housing, with residential investment contracting sharply. Consumer spending has remained resilient, however, supported by labor income growth and still-elevated savings.

As we said in the most recent FOMC statement, we anticipate “ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”11 What policy rate is sufficiently restrictive we will only learn over time by watching how the economy evolves. Given the tightening already in the pipeline, I am mindful that monetary policy works with long lags. Thus, as we get closer to that uncertain destination, it would be prudent to move in smaller steps. How far we go, and how long we keep rates restrictive, will depend on observed progress in bringing down inflation. But rest assured, we will keep at it until the job is done.

Thank you.

1. See Mehrdad Esfahani, John G. Fernald, and Bart Hobijn (2020), “World Productivity: 1996–2014,” ASU Center for the Study of Economic Liberty Research Paper (Tempe, Ariz.: Arizona State University, March). Return to text

2. See Robert J. Gordon and Hassan Sayed (2019), “The Industry Anatomy of the Transatlantic Productivity Growth Slowdown,” Working Paper 25703 (Cambridge, Mass.: National Bureau of Economic Research, March); Nicholas Bloom, Charles L. Jones, John Van Reenen, and Michael Webb (2020), “Are Ideas Getting Harder to Find?” American Economic Review, vol. 110 (April), pp. 1104–44. Return to text

3. In 1975, Gordon Moore predicted that the number of transistors found on integrated circuits (semiconductors) would double every two years. The accuracy of this prediction, known as Moore’s Law, is used as a barometer of the pace of technical advance in the electronics industry. Return to text

4. Mismeasurement could also be a contributor to the lackluster productivity gains in manufacturing. See Susan Houseman, Christopher Kurz, Paul Lengermann, and Benjamin Mandel (2011), “Offshoring Bias in U.S. Manufacturing,” Journal of Economic Perspectives, vol. 25 (Spring), pp. 111–32; David M. Byrne, John G. Fernald, and Marshall B. Reinsdorf (2016), “Does the United States Have a Productivity Slowdown or a Measurement Problem?” Finance and Economics Discussion Series 2016-017 (Washington: Board of Governors of the Federal Reserve System, March). Return to text

5. According to the Quarterly Survey of Plant Capacity, over 40 percent of manufacturers report difficulty hiring workers, triple the rate before the pandemic. The Association for Advancing Automation reports that as of 2022:Q3, orders were 50 percent higher than two years earlier. Return to text

6. See David H. Autor (2015), “Why Are There Still So Many Jobs? The History and Future of Workplace Automation,” Journal of Economic Perspectives, vol. 29 (Summer), pp. 3–30; Daron Acemoglu and Pascual Restrepo (2020), “Robots and Jobs: Evidence from U.S. Labor Markets,” Journal of Political Economy, vol. 128 (June), pp. 2188–244; Gilbert Cette, Aurélien Devillard, and Vincenzo Spiezia (2021), “The Contribution of Robots to Productivity Growth in 30 OECD Countries over 1975–2019,” Economics Letters, vol. 200 (March). Return to text

7. See Erik Brynjolfsson, Daniel Rock, and Chad Syverson (2021), “The Productivity J-Curve: How Intangibles Complement General Purpose Technologies,” American Economic Journal: Macroeconomics, vol. 13 (January), pp. 333–72. Return to text

8. See Paul A. David (1990), “The Dynamo and the Computer: An Historical Perspective on the Modern Productivity Paradox,” American Economic Review, vol. 80 (May), pp. 355–61. Return to text

9. The relationship between competition and innovation is complicated and a matter of some debate. See Philippe Aghion, Nick Bloom, Richard Blundell, Rachel Griffith, and Peter Howitt (2005), “Competition and Innovation: An Inverted-U Relationship,” Quarterly Journal of Economics, vol. 120 (May), pp. 701–28. In addition, see the discussion of the literature in Rachel Griffith and John Van Reenen (2021), “Product Market Competition, Creative Destruction and Innovation,” CEPR Discussion Paper No. DP16763 (Washington: Center for Economic and Policy Research, November). Return to text

10. See Ryan Decker, John Haltiwanger, Ron Jarmin, and Javier Miranda (2014), “The Role of Entrepreneurship in U.S. Job Creation and Economic Dynamism,” Journal of Economic Perspectives, vol. 28 (Summer), pp. 3–24. Return to text

11. See Board of Governors of the Federal Reserve System (2022), “Federal Reserve Issues FOMC Statement (PDF),” press release, November 2. Return to text

คำแนะนำการอ่านบทความนี้ : บางบทความในเว็บไซต์ ใช้ระบบแปลภาษาอัตโนมัติ คำศัพท์เฉพาะบางคำอาจจะทำให้ไม่เข้าใจ สามารถเปลี่ยนภาษาเว็บไซต์เป็นภาษาอังกฤษ หรือปรับเปลี่ยนภาษาในการใช้งานเว็บไซต์ได้ตามที่ถนัด บทความของเรารองรับการใช้งานได้หลากหลายภาษา หากใช้ระบบแปลภาษาที่เว็บไซต์ยังไม่เข้าใจ สามารถศึกษาเพิ่มเติมโดยคลิกลิ้งค์ที่มาของบทความนี้ตามลิ้งค์ที่อยู่ด้านล่างนี้

Source link

{kind=link}

{kind=link}